Ten Years Later: The Lasting Impact of Protecting Fixed Indemnity Coverage

Over the past decade, the American healthcare landscape has continued to evolve. Rising healthcare costs, increasing deductibles and growing out-of-pocket expenses have changed the way individuals and families prepare for unexpected medical events.

But while healthcare has transformed in many ways, one principle has remained just as important today as it was ten years ago: giving consumers the freedom to choose coverage that fits their unique needs.

July 2026 marks the 10th anniversary of the historic Central United Life Insurance Co. v. Burwell decision, a ruling that helped preserve consumer access to fixed indemnity coverage, including fixed indemnity insurance products designed to provide supplemental financial protection.

In 2016, at the time of the judgement, ManhattanLife was operating as Central United Life. With decades of achievement to its name, our organization now operates as ManhattanLife, honoring our past and the history we continue to make, as we help safeguard the rights of American policyholders.

Although this case centered on federal healthcare regulations, its lasting impact reaches far beyond the court of law.

For millions of Americans, it helped ensure continued access to supplemental coverage designed to provide financial support when it matters most.¹

A Decade of Consumer Protection

Hospital indemnity insurance is designed to complement major medical coverage by providing fixed cash benefits when a covered hospitalization occurs. Rather than paying medical providers directly, these benefits are generally paid to the policyholder, who can use the funds however they choose.

Consumers today often face significant deductibles, coinsurance and other out-of-pocket expenses before their primary health insurance begins paying the full cost of care. Even routine hospital stays can create financial strain and the impact frequently goes even further than medical bills, adding up to a veritable mountain of expenses such as:

- Lost Wages

- Childcare

- Transportation

- Lodging

- Groceries

- Rent

The continued demand for alternative or supplemental health coverage reflects these realities. According to industry data, workplace supplemental health insurance sales, including hospital indemnity, accident, critical illness, and cancer insurance, reached approximately $2.6 billion in new annualized premium through the first three quarters of 2024, representing a 10% increase over the same period in 2023.²

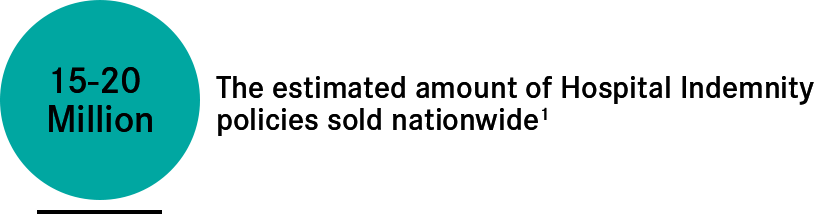

Based on industry averages for hospital indemnity premiums and market growth, it is estimated that 15 to 20 million hospital indemnity policies have been purchased nationwide since the 2016 decision.

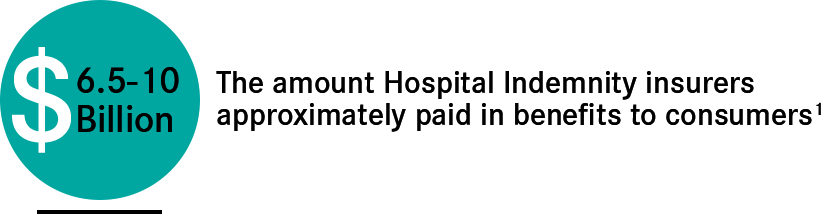

During that same period, these products have likely paid an estimated $6.5 to $10 billion in cash benefits directly to consumers, helping individuals and families manage both medical expenses and the everyday financial obligations that do not stop during a health event.³

Why Consumer Choice Still Matters

The healthcare needs of every individual and family can differ widely. A young professional may be focused on protecting their savings from an unexpected accident. Parents may want additional financial support should a family member require hospitalization. Someone approaching retirement may simply want greater peace of mind.

But one-size-fits-all solutions rarely address every financial concern.

Hospital indemnity insurance, as part of fixed indemnity coverage, allows consumers to personalize their financial protection by adding coverage that works alongside their existing health insurance toward hospital related incidents. Instead of replacing major medical coverage, these policies are designed to help fill financial gaps that traditional health plans may leave behind.

The Central United Life Insurance Co. v. Burwell decision reinforced this distinction.

By affirming that fixed indemnity insurance serves a different purpose than comprehensive medical coverage, the ruling helped preserve an important option for consumers seeking additional financial protection.¹

Looking Ahead

Healthcare will continue to change. Costs will fluctuate, new challenges will emerge and consumer needs will develop alongside them. Yet one principle should remain constant: individuals and families should have the ability to choose coverage that reflects their circumstances, priorities and financial goals.

For over 175 years, ManhattanLife has believed that meaningful protection begins with providing people with options.

With this case, ManhattanLife once again demonstrated that our tagline isn’t just a marketing move; they are words we have pledged to live up to: Standing By You. Since 1850. The case also reminded us how much of a difference we can make for our valued customers and partners. When we talk about making history, this is what we mean. Our unwavering philosophy continues today through supplemental health products designed to help consumers prepare for life's unexpected moments.

Ten years after Central United Life Insurance Co. v. Burwell, the decision stands as more than a legal milestone for fixed indemnity coverage. It serves as a reminder that preserving consumer choice extends beyond an insurance policy or legal regulation. It is about empowering millions of Americans to make informed decisions, strengthen their financial resilience and navigate an increasingly complex healthcare system with greater confidence and peace of mind.

Learn more about this landmark case and what it still means for consumers by visiting our landing page.

Get in Touch

Works Cited

1. Bloomberg Law. “When Agencies Color Outside the Lines: Implications of Central United Life Inc. v. Burwell.” Bloomberg Law, 2015. https://news.bloomberglaw.com/health-law-and-business/when-agencies-color-outside-the-lines-implications-of-central-united-life-inc-v-burwell

2. Insurance Forums. “Workplace Supplemental Health Sales Up 10% Through Q3 2024.” Insurance Forums, 2024. https://www.insurance-forums.com/employee-benefits/group-health/workplace-supplemental-health-sales-up-10-through-q3-2024/

3. Telos Actuarial. “Hospital Indemnity Growth.” Telos Actuarial, 2024. https://www.telosactuarial.com/blog/hospital-indemnity-growth