The Power of Tax-Deferred Annuities for Long-Term Growth

What Do Tax-Deferred Annuities Mean?

Tax-deferred annuities allow your investments to grow without being reduced by annual taxes, making them a powerful tool for long-term financial planning. The concept can be likened to a greenhouse, where plants can grow freely, without harsh weather or other factors slowing them down. They get bigger and stronger over time because nothing is constantly inhibiting their growth. That’s how tax-deferred growth works: your money compounds without yearly taxes trimming it back.

With tax-deferred annuities, earnings such as interest and gains accumulate without immediate taxation, giving your investment more room to mature. This process, known as deferred annuity taxation, allows you to delay paying taxes until withdrawals are made, helping you make the most of your long-term savings’ goals.

How Tax-Deferred Annuities Grow Through Compound Interest

One of the most compelling advantages of tax deferral is how it enhances compounding. Because your earnings aren’t reduced annually by taxes, the full value of your investment continues working for you. Over time, this uninterrupted growth can lead to significantly greater accumulation compared to taxable alternatives. If you are seeking low-risk investments, this key benefit makes annuities an efficient and dependable way to build wealth.

Because your earnings aren’t reduced annually by taxes, the full value of your investment continues working for you.

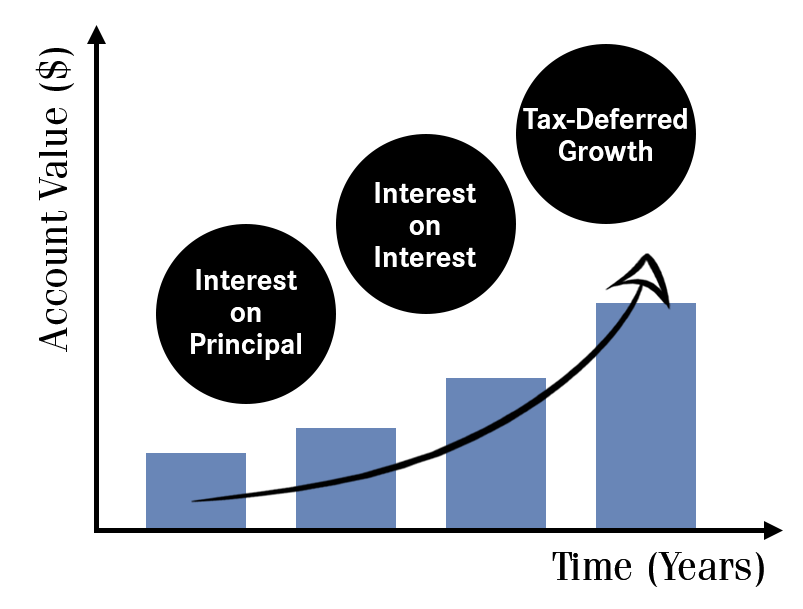

Let’s consider a comparison. If you have a Certificate of Deposit (CD) at a bank and you put in $10,000 at the beginning of the year at 3% interest, at the end of the year, you will have $10,300 dollars. That is a great sum of money! However, the following year, you still have to pay taxes on the interest earned, which is $300. Conversely, an annuity, which is typically tax deferred, functions differently as it involves triple compounding. This is how it works:

- In Year 1: You earn interest on your principal (the amount of money you originally put in).

- In Year 2: You earn interest on your principal plus Year 1’s interest. That’s interest on top of interest.

- In Year 3+: Your money keeps growing.*

* Interest is credited and compounded daily to arrive at an effective yield.

As the graphic below shows, the result is a larger sum of money to help you feel more confident about your retirement income and financial future.

Understanding Your Options: Fixed vs. Variable Annuities

Tax-deferred growth is available across different types of annuities, primarily fixed and variable. When considering a fixed annuity versus a variable annuity, the major distinction lies in risk tolerance and return expectations. A tax deferred fixed annuity offers guaranteed growth and predictable outcomes, while variable annuities provide market-based returns with the potential for higher gains and greater fluctuation. Both, however, fall under the umbrella of tax-deferred annuities and share the same tax advantages.

When considering a fixed annuity versus a variable annuity, the major distinction lies in risk tolerance and return expectations.

Multi-Year Guarantee Annuities (MYGAs)

A multi-year guarantee annuity (MYGA) is a type of fixed annuity designed to provide a guaranteed interest rate over a set period, usually ranging from 3 to 10 years. This means your money grows at a steady, predictable pace without being affected by market fluctuations, making it a strong choice for those looking for stability and low risk. In addition, MYGAs offer tax-deferred growth, allowing your earnings to compound over time without being reduced by annual taxes.

Timing Taxes to Your Advantage

Another benefit of tax-deferred annuities is the flexibility they offer in managing when you pay taxes. Withdrawals are often made during retirement, when many individuals may be in a lower tax bracket. This timing can help reduce the overall tax burden, making tax deferral not just a growth strategy, but an economical tax-planning tool as well.

What to Remember about Tax Deferral and Annuities

When it comes to tax deferral and annuities, it is important to keep in mind that taxes are still due when you withdraw the income, even if those withdrawals are spread out over time, since the gains are often taxed as ordinary income. Because of this structure, annuities are best viewed as a long-term financial opportunity rather than a short-term savings option. If you are planning for immediate or short-term needs, such as purchasing a car or funding a child’s college education, annuities may not be the most suitable due to potential withdrawal restrictions, timing considerations and tax implications.

Additionally, annuities are considered insurance and not a traditional investment. There is also less liquidity than short-term investments. But they do offer a financial opportunity that typically involves less risk with more guarantees.

A Practical Approach to Long-Term Savings

Ultimately, tax-deferred annuities combine growth potential with tax efficiency and stability. Whether you consider purchasing a MYGA or another type of fixed annuity, by allowing your money to compound without immediate tax impact, you can benefit from a strong foundation for long-term financial planning.

Remember, you don’t invest to make less, you invest to make more. That is a key concept behind annuities. For individuals looking to balance steady growth with smart tax strategies, tax-deferred annuities remain a practical and effective solution.

To learn how tax-deferred annuities from ManhattanLife can help support your savings’ goals, visit our Annuities web page.