The Value of Bundling Supplemental Policies in Employer-Sponsored Benefits Programs

Bundling health policies has gained traction in modern employer-sponsored benefits programs, making simplicity as important as coverage itself. When employees are presented with multiple standalone supplemental insurance policies, even valuable benefits like hospital indemnity insurance, critical illness insurance and accident insurance can feel fragmented or difficult to fully appreciate. Bringing these voluntary benefits together creates a more cohesive structure that’s easier to understand and act on.

Why Bundling Supplemental Policies Matters

The real upside to bundling voluntary benefits is clarity. When supplemental health benefits are packaged in a more unified way, employees are more likely to recognize their value and engage with them during enrollment. That matters in today’s competitive benefits landscape, especially when more than 85% of organizations say they see a positive impact on employee satisfaction as a result of their benefits program, with supplemental benefits amplifying that effect.¹

By combining hospital indemnity insurance, critical illness insurance and accident insurance into cohesive bundled insurance benefits, employers can simplify decision-making, improve engagement and enhance financial protection for employees. The following expands on bundling policies, explaining what it is, key benefits, applicable examples and how it supports employers and their employees.

What Is Bundling Supplemental Policies?

Bundling supplemental policies refers to the practice of grouping multiple supplemental insurance policies into a single, coordinated offering within workplace benefits programs.

For employees, this means having multiple supplemental insurance options packaged together, rather than the employer offering them individually. By doing this, employees can review, compare and enroll in a coordinated set of benefits during enrollment making it easier to explain to employees their added value. This also allows employers the advantage of offering coverage that helps fill the gaps in traditional medical coverage.

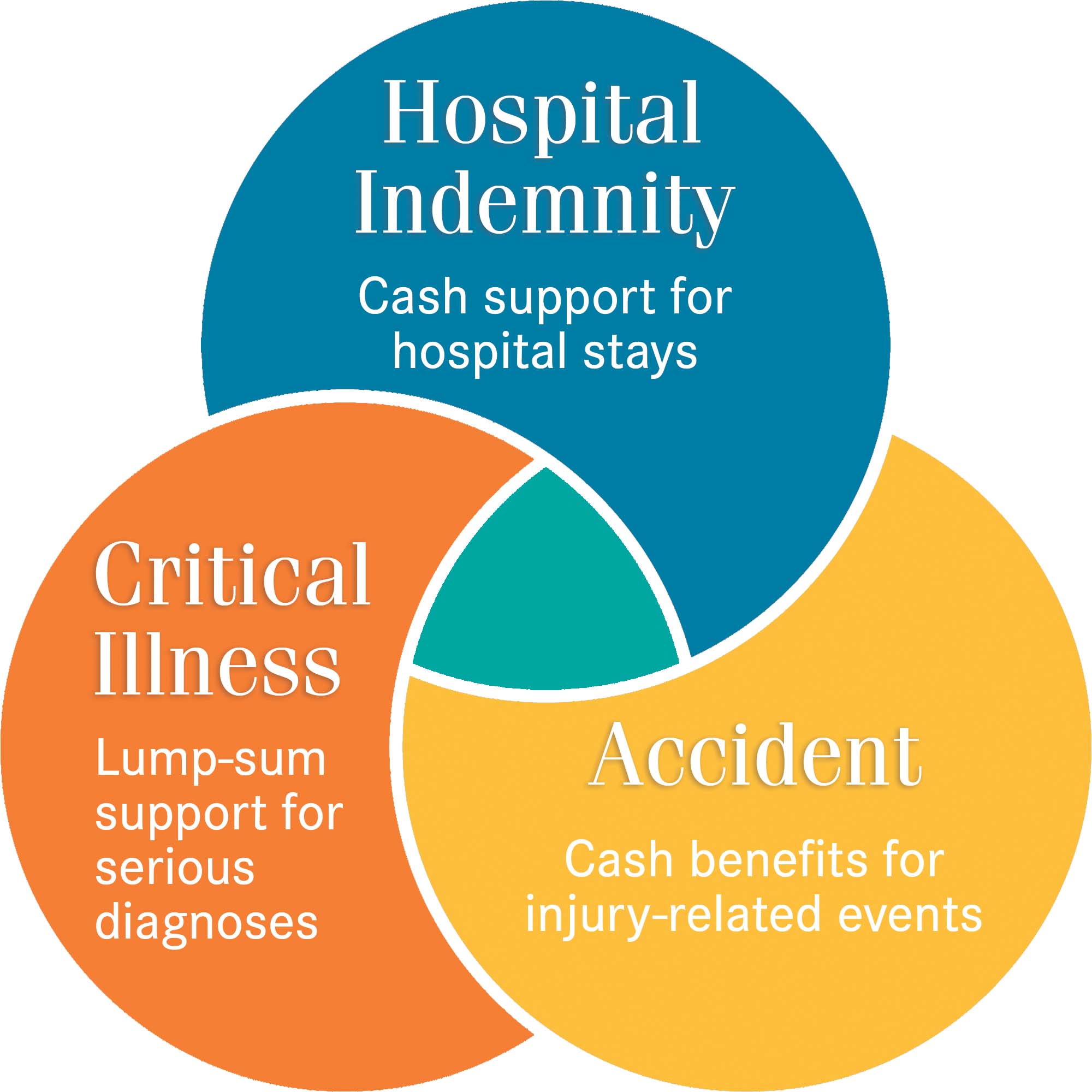

Typically ancillary coverage includes voluntary benefits such as hospital indemnity insurance, critical illness insurance and accident insurance. Each of these is designed to provide cash benefits that help employees manage out-of-pocket costs during health-related events.

Key Benefits of Bundling Supplemental Policies for Employee Benefits

One of the primary advantages of bundling supplemental policies is improved employee awareness of their offering and increased participation. When benefits are simplified into a cohesive package, employees are more likely to engage with their supplemental health benefits and make informed decisions. This matters because adoption of voluntary benefits remains uneven as recent data suggests.

Industry research indicates that only about 11% of employers currently offer the full trio of accident, critical illness and hospital indemnity insurance.1

From an employer standpoint, bundling enhances the value of employer-sponsored benefits by streamlining administration and improving communication. It also strengthens overall workplace benefits programs, helping employers differentiate themselves in competitive labor markets where benefits play a major role in talent attraction.

Essentially, bundling group hospital indemnity, critical illness and accident coverage creates a more complete employee-sponsored benefits strategy because each product addresses a different financial need while working together cohesively.

Hospital indemnity helps with costs associated with inpatient hospital stays or post-confinement, critical illness provides lump-sum support for serious diagnoses such as cancer, vascular conditions such as heart attack and other critical illnesses, while accident coverage helps offset expenses tied to unexpected injuries.

Summarily, they create layered financial protection that can help employees better manage the real costs of a medical event.

How Voluntary Benefits Can Offset a High-Deductible Health Plan

This combination is especially valuable alongside a High-Deductible Health Plan (HDHP), where out-of-pocket costs can quickly become overwhelming. Rather than overlapping, the products complement one another by filling different financial gaps while also simplifying enrollment and payroll deductions through one bundled offering. The result is a streamlined voluntary benefits benefits package that helps employees feel more financially prepared when the unexpected happens.

What Is an Example of Bundled Supplemental Policies?

A common example of bundled supplemental policies includes combining hospital indemnity insurance, critical illness insurance and accident insurance into a single offering. However, as stated previously, employers can offer employees each of these as separate products or even pair two or three of them together.

Bundling these products works well because it reflects how real-life events actually happen, rarely in isolation and often in different ways across a family. An accident plan might help cover something as common as a child’s sports or playground injury, while a more serious car accident could trigger both accident and hospital indemnity benefits if inpatient confinement is required. In more severe cases, like a stroke, critical illness coverage provides a lump-sum benefit, which can be further supported by Hospital Indemnity if there is an extended hospital stay.

A family example also helps show how these products complement rather than duplicate each other. One household might experience multiple separate events, a cancer diagnosis for one parent, an accident involving a child, and an unrelated injury to the other parent. Each of these events activates different benefits across the three coverages.

The goal isn’t that all three products always work together at once, but that they collectively ensure protection across a wide range of unexpected situations, helping individuals and families stay financially supported no matter what type of event occurs.

Why Bundling Supplemental Policies Matters for Brokers

Bundling allows brokers to focus less on individual products and more on solving broader financial protection gaps. From a broker perspective, group supplemental products create real value for employers when they’re positioned as part of a broader benefits strategy rather than standalone offerings.

While voluntary benefits alone may not be the primary driver of recruitment, they add meaningful depth to a workplace benefits program and may help strengthen retention.

The larger opportunity comes when employers evaluate plan design, particularly moving from a traditional PPO structure to a High-Deductible Health Plan (HDHP) supported by supplemental coverage that helps offset out-of-pocket costs. In many cases, this combined approach can reduce overall employer spend while still enhancing employee protection and financial security.

When brokers take a consultative, full-benefits approach, the conversation shifts toward total plan design rather than individual products. Supplemental benefits like hospital indemnity, critical illness and accident coverage can be layered with HDHP plans to help fill financial gaps and create a more sustainable long-term solution. This approach is less transactional and more relationship-driven, centered on understanding the group’s range of needs.

How Bundled Supplemental Policies Support Employers and Employees

For employers, bundled insurance benefits provide a competitive advantage in designing stronger employer-sponsored benefits packages. They help improve employee attraction and retention while reducing confusion around multiple plan options. Bundling also supports more efficient communication of workplace benefits programs, allowing HR teams to present a better integrated and more practical benefits package.

For employees, the impact is even more direct. Bundled supplemental health benefits create a more complete safety net during unexpected medical events, helping cover expenses that traditional insurance may not fully address. Whether facing a hospital stay, a serious illness or an accident, employees gain access to coordinated financial support that can reduce stress and help facilitate a healthy work environment.

Conclusion

Ultimately, bundling supplemental policies represents a meaningful evolution in how organizations design supplemental insurance policies within modern employer-sponsored benefits programs.

By combining hospital indemnity insurance, critical illness insurance and accident insurance into cohesive bundled insurance benefits, employers can simplify decision-making, improve engagement and enhance financial protection for employees.

As demand for supplemental health benefits keeps building, the option to bundle is proving to be one of the most effective ways to strengthen overall workplace benefits programs for small and large organizations.

To learn more about ManhattanLife’s employer Group Accident, Group Critical Illness and Group Hospital Indemnity plans and other Voluntary Benefits, please visit: please visit our web page.

Get in Touch

Works Cited

1. Employee Benefit Research Institute (EBRI). “Expanding the Benefits Horizon: How Employers View Voluntary Offerings.” https://www.ebri.org/content/expanding-the-benefits-horizon--how-brokers-view-voluntary-offerings